In today's fast-paced financial world, the choice between credit and debit cards can significantly impact your spending habits and financial health. Both card types serve different purposes and come with unique benefits and drawbacks. Understanding these differences is essential for making informed financial decisions that align with your lifestyle and goals.

As consumers, we often face the dilemma of which card to use for our purchases. A credit card allows you to borrow money up to a certain limit, while a debit card deducts funds directly from your bank account. This fundamental difference can influence not only your spending behavior but also your credit score and financial flexibility.

In this article, we will delve deep into the distinctions between credit and debit cards, exploring their advantages and disadvantages, which will equip you with the knowledge to make wiser financial choices. Let’s embark on this journey to unravel the complexities of credit vs debit!

Table of Contents

- 1. What is a Credit Card?

- 2. What is a Debit Card?

- 3. Key Differences Between Credit and Debit Cards

- 4. Advantages of Using Credit Cards

- 5. Advantages of Using Debit Cards

- 6. Potential Risks of Credit and Debit Cards

- 7. How to Choose the Right Card for You

- 8. Conclusion

1. What is a Credit Card?

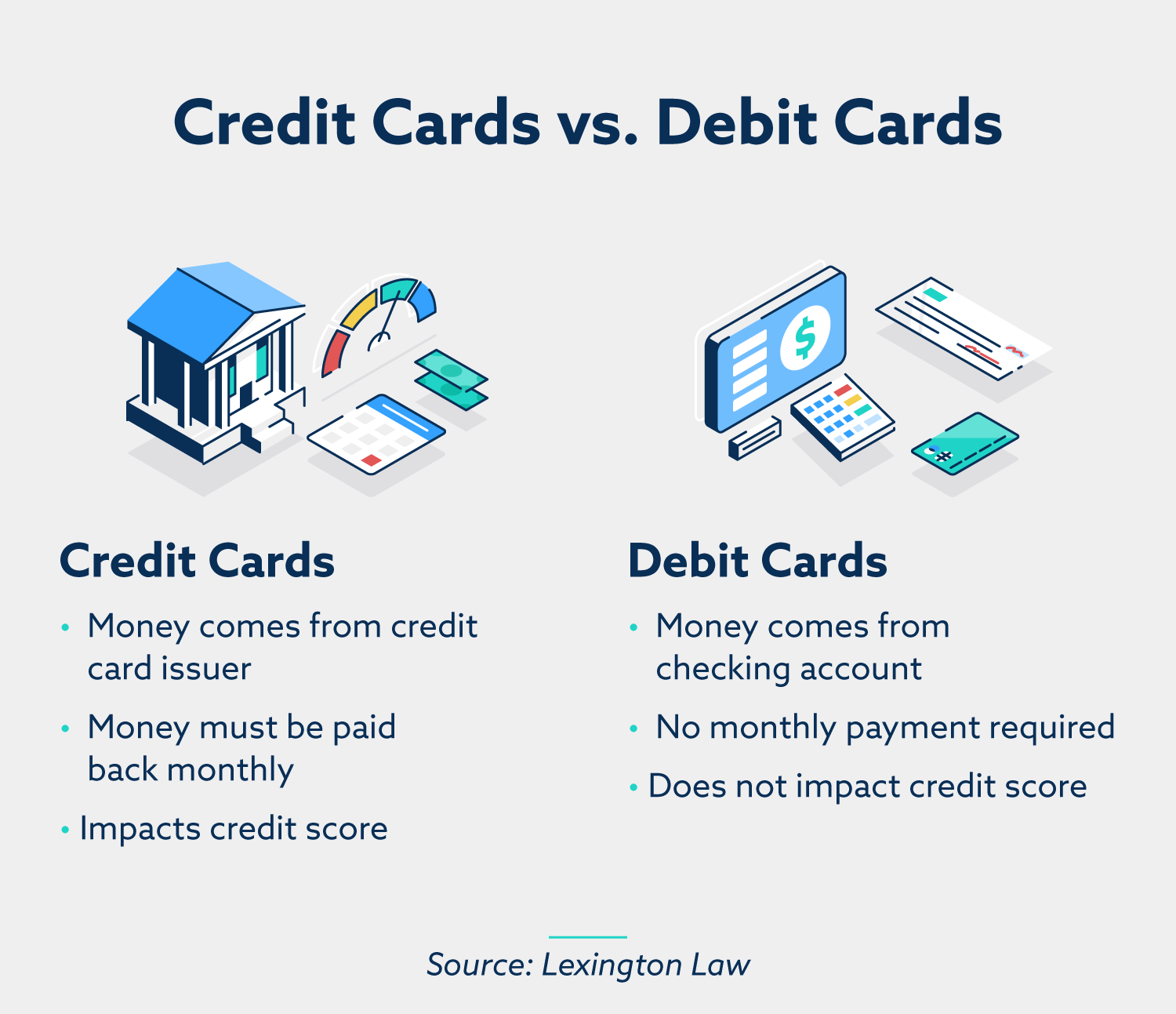

A credit card is a financial tool that allows you to borrow money from a lender up to a specific limit to make purchases or withdraw cash. You are expected to pay back the borrowed amount, usually on a monthly basis, along with interest if the full balance is not paid. Credit cards often come with various benefits such as rewards programs, cash back, and travel perks.

1.1 Features of Credit Cards

- Borrowing Limit: Set by the credit card issuer based on your creditworthiness.

- Interest Rates: Vary based on your credit score and payment history.

- Rewards Programs: Many credit cards offer points, miles, or cash back on purchases.

- Credit Score Impact: Responsible use can help build your credit score.

2. What is a Debit Card?

A debit card is linked directly to your bank account and allows you to access your funds for purchases or cash withdrawals. When you use a debit card, the money is immediately deducted from your checking account, making it easier to manage your budget and avoid overspending.

2.1 Features of Debit Cards

- No Borrowing: You can only spend what you have in your bank account.

- No Interest Rates: Since you are using your own money, there are no interest charges.

- ATM Access: Debit cards can be used to withdraw cash from ATMs.

- Limited Rewards: Fewer debit cards offer rewards compared to credit cards.

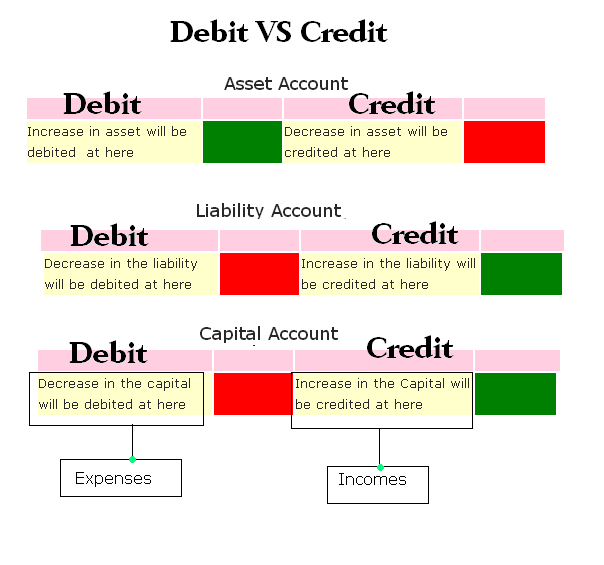

3. Key Differences Between Credit and Debit Cards

Understanding the key differences between credit and debit cards can help you choose the right one for your needs. Here are some crucial aspects to consider:

3.1 Payment Method

Credit cards allow you to borrow money, while debit cards require you to use your own funds. This fundamental difference affects how you manage your finances.

3.2 Impact on Credit Score

Using a credit card responsibly can build your credit score, whereas debit card usage does not affect your credit score at all.

3.3 Fees and Interest Rates

Credit cards may come with annual fees and interest charges, while debit cards typically have lower fees, often no annual fees or interest.

3.4 Fraud Protection

Credit cards generally offer better fraud protection compared to debit cards, as consumers are not liable for unauthorized charges if reported promptly.

4. Advantages of Using Credit Cards

Credit cards can offer numerous benefits for users who understand how to manage them effectively:

- Rewards and Bonuses: Many credit cards offer points or cash back for purchases.

- Extended Warranty: Some cards provide extended warranty benefits for purchased items.

- Travel Perks: Credit cards often include travel insurance, rental car insurance, and no foreign transaction fees.

- Emergency Funds: In case of an emergency, a credit card can provide quick access to funds.

5. Advantages of Using Debit Cards

Debit cards also have their own set of advantages, especially for those who prefer to spend within their means:

- Budget Control: Since you can only spend what you have, it's easier to manage your budget.

- No Debt Accumulation: Debit cards help you avoid the risk of accumulating debt.

- Lower Fees: Debit cards generally have fewer fees than credit cards.

- Immediate Transactions: Transactions are processed immediately, allowing for real-time tracking of your expenses.

6. Potential Risks of Credit and Debit Cards

While both credit and debit cards offer benefits, they also carry certain risks that users should be aware of:

6.1 Risks of Credit Cards

- Debt Accumulation: High credit card debt can lead to financial stress and lower credit scores.

- High-Interest Rates: If balances are not paid in full, interest can accumulate quickly.

- Fraud Risk: Although protected, unauthorized charges can still occur.

6.2 Risks of Debit Cards

- Limited Fraud Protection: Users may face greater liability for unauthorized transactions.

- Overdraft Fees: Spending more than your account balance can lead to fees.

- Less Control Over Funds: If your card information is compromised, your entire account may be at risk.

7. How to Choose the Right Card for You

Choosing between a credit card and a debit card depends on your financial habits and goals. Consider the following:

7.1 Assess Your Spending Habits

If you are disciplined with spending and can pay off balances, a credit card may offer more benefits. If you prefer to stick to a budget, a debit card might be the better choice.

7.2 Evaluate Your Financial Goals

Consider your long-term financial goals. If building credit is essential, opt for a credit card. If you want to avoid debt, a debit card is the way to go.

7.3 Look for Additional Benefits

Research the benefits each card offers and choose one that aligns with your lifestyle, whether it’s rewards, travel perks, or low fees.

8. Conclusion

In summary, understanding the differences between credit vs debit cards is crucial for making informed financial decisions. Both card types have their advantages and disadvantages, and the right choice ultimately depends on your individual financial habits and goals.

As you consider your options, think about what matters most to you—whether it’s rewards, spending control, or credit building. Remember to use your chosen card responsibly to maximize its benefits. If you found this article helpful, please leave a comment, share it with others, or explore additional articles on our site for more financial insights!

References

- Consumer Financial Protection Bureau. (n.d.). consumerfinance.gov

- National Foundation for Credit Counseling. (n.d.). nfcc.org

Thank you for reading! We hope this article helps you navigate the world of credit and debit cards more effectively. We look forward to welcoming you back for more informative content in the future!

You Might Also Like

Tom Berenger's Wives: A Journey Through Love And LifeThe Ultimate Guide To HIBIDF: Understanding And Navigating The World Of HIBIDF

Jocelyn Wildenstein: The Life And Transformation Of The Catwoman

Discovering Justin Pasutto: Age, Biography, And More

Unveiling The Life And Legacy Of Dallas McAver

Article Recommendations

- Gal Gadots Husband A Closer Look At Yaron Varsano

- Importance Of Privacy For Celebrities Shiloh Joliepitts Journey

- Twin Brother Of Interior Designer David Bromstad Meet His Sibling